Insurance is essential for home construction projects. It’s the backbone for protecting one of your biggest investments – your new home.

It’s important to go into the construction process with a good understanding of what’s covered and what’s not. Here’s a guide to help you understand insurance during the construction of your home:

What’s Important About Insurance During Homebuilding?

Insurance may be at the bottom of your to-do list when it comes to building your new home, but you should talk to an insurance agent before your construction plans are set in stone. This way, you can be positive that the location or details of your home don’t cause a problem with insurance. For example, building in a flood zone may come with higher premiums. If you have the opportunity to find a different location before you’re stuck with higher insurance costs, it can save you in the long run.

Unoccupied property poses risks for different problems than occupied property does. This is why coverage is important: it will protect your property before it’s occupied.

Homeowner’s Insurance

A standard homeowner’s insurance policy will cover damage to the structure as it’s being built, but there are some gaps that it may not cover (that’s where builder’s risk insurance comes in – to cover the gaps that your homeowner’s policy may miss – but we’ll elaborate on that in a second).

Your homeowner’s insurance will also include liability coverage, so you’ll be safe in the event that someone gets injured on the property before the home is completed. However, the policy will not cover personal property until the home is secure or lockable. After that point, you can add coverage for your personal property. If you own the property prior to the beginning of construction, be sure to get liability coverage on the property.

One important bonus about building a home is that your insurance policies will most likely be discounted. Choosing fire-resistant materials (like brick over vinyl siding) can also lead to savings on insurance. One of the biggest factors that plays into the cost of your policy is the location of your home. According to Insure.com, the home must be within 1,000 feet of a fire hydrant or within 5 miles from the nearest fire station for preferred rates. You may pay a higher premium for rural locations that don’t fall within those boundaries. For homes that do fall outside those boundaries, adding a sprinkler system may help keep your insurance costs down.

Some insurance agencies even offer discounts for extended periods, starting with the highest discount in the first year and decreasing each year after. This means that you’ll have a brand new home and still spend less on homeowner’s insurance than you would if you bought an older home.

Builder’s Risk Insurance

Builder’s risk insurance (also known as course of construction insurance) covers materials that are in transit AND what is onsite. It will cover a variety of situations, including fire, wind, theft, vandalism, and negligence. With Reinbrecht Homes, builder’s risk insurance is included in the price of the home.

Builder’s risk policies vary for every build because no two builds are exactly the same. For example, hurricanes may be covered in coastal areas, while hurricane coverage wouldn’t be necessary for land-locked areas. Builder’s risk insurance begins on the policy effective date and ends whenever construction is completed. In the rare case that the timeline for the build gets extended, there are extensions available for builder’s risk insurance.

Faulty design, materials, and workmanship typically aren’t covered by builder’s risk insurance since those are often the result of professional error. Extreme events, like floods or earthquakes, may also be excluded from coverage. If the project is in a flood zone or near a fault line, the insurance carrier may have a supplemental policy to cover events like this.

Why the Right Coverage is Important

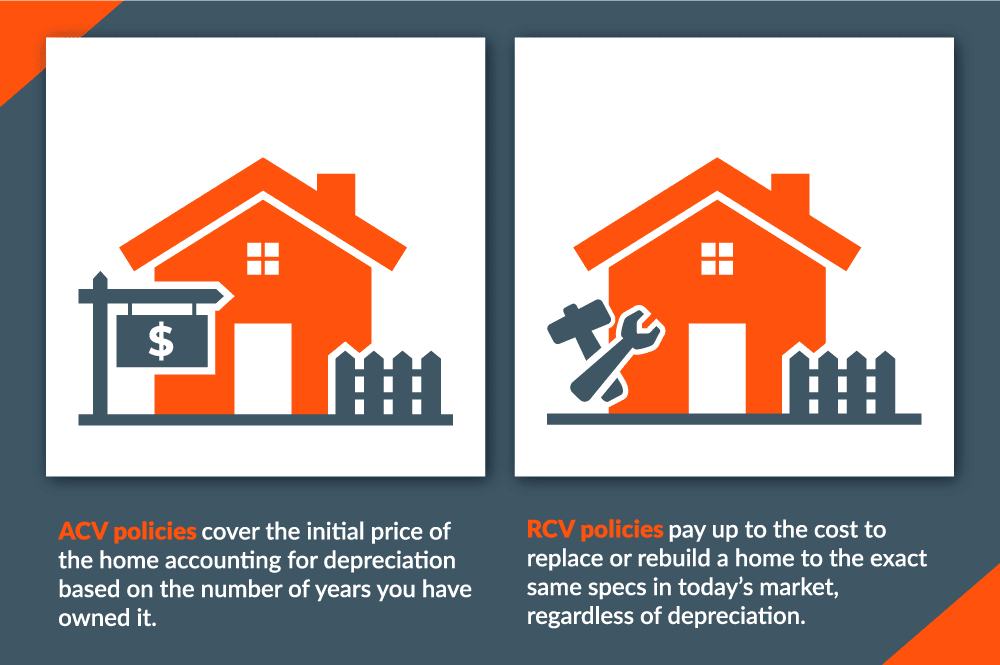

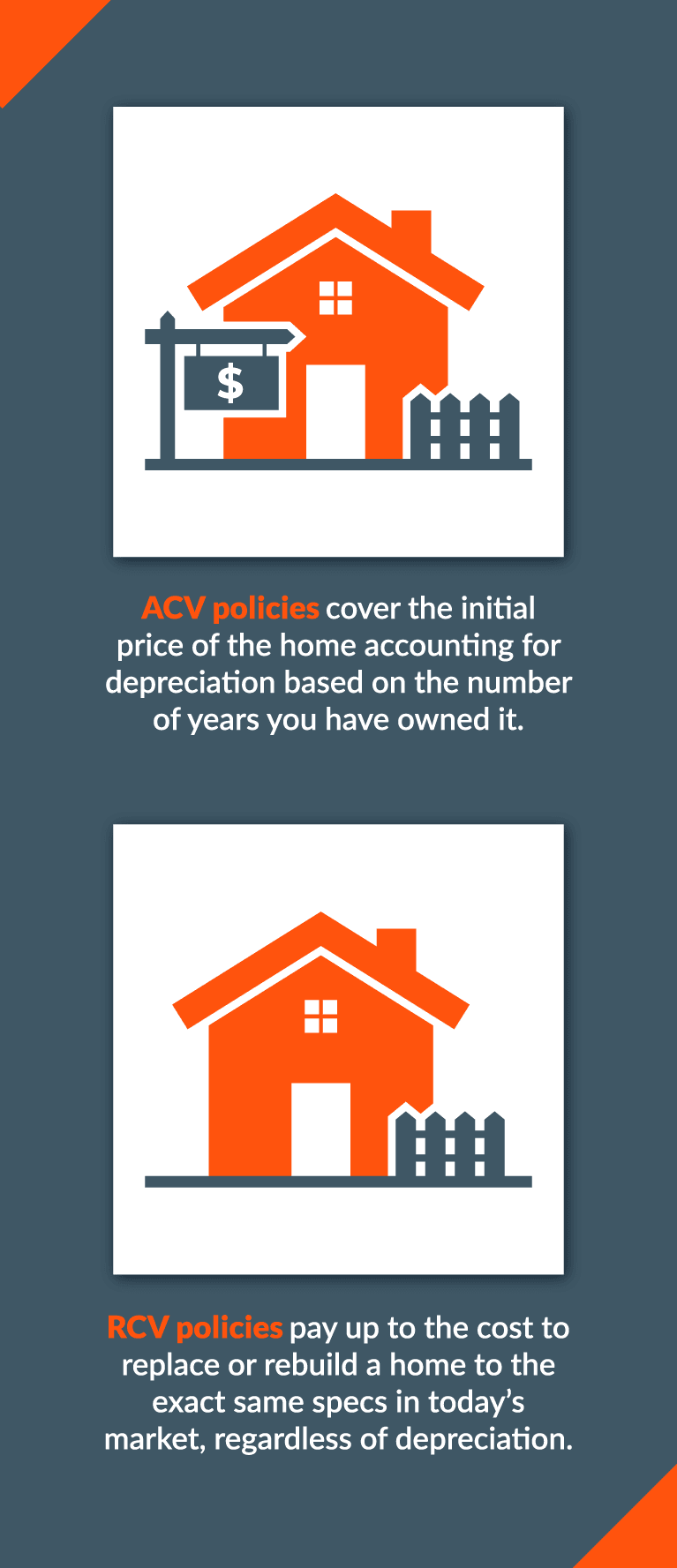

There are two types of homeowner’s coverage you see are Actual Cash Value (ACV) and Replacement Cost Value (RCV). ACV policies cover the initial price of the home accounting for depreciation based on the number of years you have owned it. RCV policies pay up to the cost to replace or rebuild a home to the exact same specs in today’s market, regardless of depreciation.

In the unhoped-for event that something does happen to your home, ACV policies will not provide you with the amount you’ll need to rebuild your home. On the other hand, RCV policies will allow you to build a home as nice as the one you had and build it to current codes. Proper insurance coverage is a vital part of homeownership, and that’s why we recommend RCV policies.

Homes under construction have more factors to cover than existing homes do. Since the building site isn’t secure, there’s a risk for tools, equipment, and materials to be stolen or vandalized. This is one example of a factor that exists during the build but not after it’s complete.

Factors like this are why it’s important to have the right coverage before construction begins. At Reinbrecht Homes, insurance during homebuilding is included in the price of your home. To learn more about what else is included in the price of your home, download our standards guide.